It has certainly been a while since my last post. Since my recent call out, the S&P 500 index has risen 2.89%, with that of the VIX index declining by more than -16%, and SVXY being up 10.66%. I am in no way bragging on how I can "time the market", because this is not entirely possible. I am simply showing the benefits of using objective information gained from within the volatility asset class, as well as the various derivatives markets that I look at, to create a probability-weighted decision-making process. Now, I will show my reasons as to why the short volatility trade might be put on pause for the near future.

Update on Market Positioning

As I have explained numerous times before, I most heavily weight the net positioning of Dealers/Intermediaries more than other categories, simply because I believe that this group has the best shorter-term information available, whether that be in pricing the implied volatility curve, or analyzing order flow. Below is a chart of net positioning of a variety of market participants. This data is on the E-Mini S&P 500 futures contracts.

Net positioning of market makers has not changed drastically on this particular derivative contract, with net long, short, and spreading positioning of dealers being up +16.28%, -15%, and +16.98%, respectively relative to 5/4/2021. For comparison's sake, Leveraged Funds (primarily CTAs or Hedge Funds) are positioned more bearishly, with net positioning of long, short, and spreading being -15.26%, +11.03%, and +5.25%, respectively, since 5/4/2021. So, the primary participant that I personally acknowledge to have the best near-term information on market movements has positioned to have increasing exposure to bullish movements within the ES futures contracts complex.

On another note, let us analyze historical positioning of Market Makers, Leveraged Funds, and Non-Commercial (market participants that are more speculative in nature, are not primarily hedging risk exposures with the particular contract) on VIX futures contracts. For those that are unaware, the VIX index measures the aggregate implied volatility of the stocks within the S&P 500 for an interpolated 30-day maturity. An interesting thing to note is how the VIX index includes a significant contribution of out-of-the-money options, making the VIX index more susceptible to movements in the "wings" of the options chain, and therefore a more appropriate measure of aggregate implied volatility across the surface (it does not include in-the-money options), but I digress. VIX futures are the respective futures contracts that track the VIX index (I have referenced them before in this blog), and they naturally converge to the cash index, the VIX index. So, a long position in the VIX future suggests the market participant desires a long exposure to implied volatility via a futures contract, and vice versa for a short position. Dealer positioning within the VIX futures complex for long, short, and spreading positioning is +50.05%, +38.19%, and +70.30%, respectively, since 12/20/2020, as of 6/15/2021. Leveraged Funds positioning for long, short, and spreading is +63.50%, -15.13%, and +108.01%, respectively, over the same time period. Non-commercial positioning in VIX futures for long, short, and spreading positioning is +71.7%, +0.27%, and +44.37%, respectively, from 12/21/2020, as of 6/15/2021. Objectively speaking, the vast majority of market participants are desiring long exposure to implied volatility, decreasing their short implied volatility exposure (although this will almost always be higher than long implied volatility exposure due to the lucrative yields involved in junction with low rates), and increasing their spreading practices. This speaks to the relative "fear factor" prevalent within the markets, as with stocks at all-time-highs for what it seems like the 200th time this YTD. My source is CFTC.

So, what does all of this positioning data mean? Well, for the ES futures contracts (provides exposure to the S&P 500), dealer positioning is ~17% more long than they were on 5/4/2021, and Dealer, Leveraged Funds, and Non-Commercial positioning are grossly long exposure for implied volatility products via the VIX futures contracts. My interpretation is that, for the near-term, there is expectation for not only volatility, but also bullish price movements for the S&P 500. This is one of the reasons why I wish to still consider a short-volatility strategy, since demand for exposure to implied volatility is extremely one-sided (we do not want to be caught in the heard mentality), and the market participant that has, in my opinion, the best information for near-term movements, the Dealers, are anticipating bullish movements in the SPX.

Market Movements

For summary, the variety of sub-indexes within the S&P 500 are all up an incredible amount, with the S&P 500 Equal-Weighted ETF vastly outperforming. My main takeaway here is that there is not a severe "drag effect" occurring between factors (what I call "drag" is when one sector is "dragging" the other indexes forward, causing the aggregate S&P 500 ETF, SPY, to appear artificially higher). They all appear to be displaying relatively healthy market dynamics, with a large category of businesses performing extremely well. This tells me that, without doing an extensive macro analysis of the entire U.S. market (which is not the purpose of my blog posts), the market appears to be in a good condition to support longer-term growth.

Price, Volume, and Volatility Dynamics

With the S&P 500 at ATHs, as well as 30-day realized volatility being relatively low over a considerable timeframe (most recent reading of close-to-close 30 day HV is 8.78%, down -9.02% YTD ) and 30-day implied volatility (VIX index) down -40.6%, there has been a considerable decline in investor demand for insurance via derivatives on the S&P 500. Meanwhile, the VVIX index (I have covered the calculation methodology and interpretation of this index extensively in prior posts, if you are unfamiliar with this index, please refer to other posts) down only -14.15%. Let's look at this more closely and see what additional information we can gain.

This chart's purpose is to display the YTD relative difference in movement between the VIX index (remember, 30-day implied volatility of different SPX options) and the VVIX index (measures the implied volatility priced into VIX options, hence the name "implied vol-of-vol", it is calculated in the same fashion as the VIX index). What is important to note here is that, since the relative bottoming in April of the two indexes, the VVIX has appreciated 10.16%, while the VIX has gone up 2.36%. You can interpret this in a couple of ways, but my objective understanding is that jump risk premia as evidenced by implied volatility-of-volatility inherent in the VIX options are pricing more of a "jump" in asset prices than that of the VIX index. Now, the VIX index is not inherently designed to price in the same degree of jump risk premia as the VVIX index (as by construction), so interpreting the rate-of-changes of each index is crucial, especially considering what the actual construction of each index interprets of itself. Another unique point is how investors generally react more aggressively (in terms of absolute-value of magnitude) to larger deviations in returns that are negative, than large jumps in asset prices to the upside. This is reflected in the options skew of higher OTM implied volatility values for put options than that of call options, as well as in a variety of other ways. Again, this elaboration is for another post. The price of the SPY has risen 6.7% since the April lows of VVIX and VIX, with the current volume relative to the day-over-day, 1 week average, 3 week average, 1 month average, and 3 month volume average all down considerably (-8.57%, -6.25%, -12.55%, -9.13%, and -27.33%, respectively). This presents an interesting dynamic, with first-order implied volatility increasing, and jump-risk premia being priced into VIX options drastically higher than that of VIX performance, as well as the SPY over the same time period. The S&P 500 SPDR ETF, SPY, had the lowest volume levels year to date. This basically means that market breadth is thinning (volume declining), as well as a rise in multiple factors of systematic risk (VIX and VVIX). These are the opposite of the combinations one would desire if long the S&P 500. For a bullish scenario, rising price, accelerating volume, and a declining volatility complex (realized AND implied) would be optimal. However, this is only partially true at this current moment, with the price of the SPY +0.20%, +1.57%, +1.25%, +2.01%, and +9.75% on a day-over-day, 1 week, 3 week, 1 month, and 3 month basis. With a relatively stagnant market as of recent, decelerating volume, and rising systematic risk, a continued long position within the S&P 500 at this time seems less optimal.

One more quick thing on the timeseries between the VIX and VVIX; if you were to look at a weekly chart (longer-term), you would be able to see that the VIX index is beginning to break down its previous regime of higher implied volatility that was brought upon by the COVID-19 shock. However, the Implied Volatility-of-Volatility index (essential for pricing VIX options, which eventually feeds back into the pricing of SPX options) has not broken down its new regime. This suggests that the breakdown of first-order implied volatility will not come at no cost, as the risk for asset jumps increases.

The below graph depicts the spread, absolute percentage points, between implied volatility and realized volatility. As one can clearly see, implied volatility has held higher than realized volatility on a consistent basis, and is prone to "overreactions", as frequently cited by academic literature on the topic. These "overreactions" is what to look for, as mass fear and one-sided positioning for a spike in realized volatility (that drives implied volatility) presents in itself an opportunity. The short-volatility opportunity arises when there is an asymmetric reaction to a relatively small downturn within the S&P 500 (like how we saw in May 26, the SPX declined -2.15%, and the VIX rose by +26%). There exists a ~+88% 30-day implied volatility premium relative to 30-day realized volatility (this means that buying options on the S&P 500 index is pretty expensive, and would be even MORE expensive for buying put options, since there exists a significant demand for downside protection as referenced by the skew).

Another point I will make is a simple quantitative model that calculates the expected forward price of an index by the time-to-maturity of options on an underlying security, as currently priced by said options. The formula for such an equation is as follows:

Fx = Katm + (e^(rt))(Cq-Pq),

where Fx = the forward index level derived by at-the-money option prices, Katm = the closest at-the-money strike of the underlying, r = the risk-free rate of an applicable maturity of a Treasury security, t = the number of days until option expiration (our forecast timeframe), Cq = the midpoint price (bid+ask/2) of the ATM call option, Pq = the midpoint price of the ATM put option. The current forecasted S&P 500 index level as quoted by options prices 20 days from now is 4,293.38, a +0.04% increase, and the derived VIX level 21 days from now is 18.07, a +12.77% increase. There is some dislocation occurring here, as we must consider the VIX index construction now. Yes, in its computation, it heavily weights ATM options on the SPX index (of those closest to it), since it is weighted by open interest of options contracts (the ATM option displays the most equity-like characteristics for a variety of reasons, hence the largest volume/OI at this region). So, if the SPX index is projected to basically be stagnant, then there is expected to be SIGNIFICANT demand for insurance in the form of (I am assuming) put contacts.

So, with rising systematic risk, an extremely thin market in terms of breadth and liquidity, one-sided positioning for implied volatility derivatives, as well as an extremely naïve VIX and SPX projected index levels, this creates an opportunity to potentially add some short-term protection to a portfolio.

Wow is there a Ton of Choices

For this section, I will talk about the relative pricing of E-Mini S&P 500 futures contracts, which might be the most suitable for an investor who is wishing to hedge their risk by utilizing options on futures, or simply the outright future.

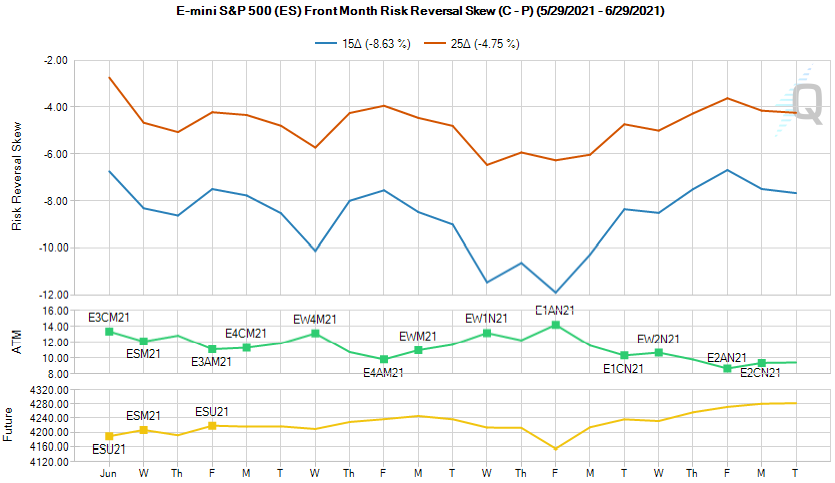

The above graph creates a visual depiction of a variety of front-month E-Mini futures contracts. The main point here is how historically "cheap" the front-month futures contract is relative to historical ATM implied volatility on said futures contract (E2CN21, 15 DTE, current ATM implied volatility of 9.47%). Front-month contracts have only been getting cheaper, and with an implied volatility value on the above particular contract representing a -43.7% discount relative to the current VIX value. Given that the VIX represents a weighted-average interpolation of 30 days, and this contract only has 15 days, it makes reasonable sense that it is cheaper, but the contract and the overall front-month complex is cheap in terms of buying insurance with positive or negative bias. In addition, the historical skew (difference in implied volatility between out-of-the-money call and put options) is relatively cheap compared to a 1 month basis. See below, as skew characteristics have not been as steep as of recent for front-month contracts.

The below graph just gives another visual representation of the skew characteristics on the current front-month contract (mentioned above).

So, now that we know that front-month implied volatility on ES futures contracts is relatively cheap, it is time to select which specific contract might best fit our needs. See the graph below.

This graph plots a smoothed, constant-maturity of 7 day, 14 day, 30 day, and 60 day ES futures contracts. So, all of the presented futures contracts are below the average ATM implied volatility, which is great. Now, remember box and whisker plots? The majority of the ES futures contracts are between the minimum value and the lower quartile, representing to be within the bottom 25% of aggregate at-the-money implied volatility across the curve of ES futures maturities. This is good, as again, they are relatively cheap. Now, for selecting which maturity, I used around 20 days in my forward index level projections, so let's keep it consistent and try to shoot for there. The previous front-month contract we analyzed was the E2CN21 ES futures contracts which expires in 15 days and is priced with an ATM implied volatility of 9.47. For only +0.43% points more, we can choose the E3AN21 ES futures contract that is priced with an ATM implied volatility of 9.90 with 20 DTE. So, a +4.45% increase in ATM price relative to a +33.33% increase in our DTE seems worth it to me. So, that contract would certainly be an option to pursue buying protection on from an ATM standpoint.

Since we are pursuing buying protection via put options in said ES futures contracts, it would be worth noting the relative level of skew, since the put options we buy would theoretically (in this specific case) be priced higher than their respective call options listed on the ES contract (as we will see holds true). Let's see how expensive put options are relative to call options (25 delta call IV - 25 delta put IV).

One can see that, time-to-maturity increases for ES contracts, the degree of skew is increased. So, the natural inclination here is to look for a contract that has a relatively cheap skew (and also not too far out in time), which would clearly be ES contact E4AN21. This contract displays a skew value of -4.26%, and is the only ES futures contract that is above the "Last" price line as given by the smoothed, constant-maturity approximation. This contract has a DTE of 27, and an ATM implied volatility of 10.34. Now, whether to play the E3AN21 ES futures contract or the E4AN21 ES futures contract is subjective. Some pricing notes to consider: for the E4AN21 contract, 27 DTE, 9.79% 25 delta call IV skew (from ATM), 14.04% delta put IV skew, -4.26% IV risk reversal (difference between the two), ATM IV of 10.34. For the E3AN21, 20 DTE, 8.32% call skew, 12.95% put skew, -4.63% risk reversal, ATM IV of 9.90.

The degree of implied volatility premium that one would pay for protection via a futures contract (in this case, for the ES_30 (constant 30-day ES futures contract)), is only +46.91% relative to 20-day historical volatility of said contract, a difference of ~31% of absolute percentage points, a significant discount as opposed to an outright bet utilizing the underlying SPX options (yes, I know that I compared the results from a 20-day HV for the ES_30 contract and a 30-day HV for the VIX, but that is the data I had. I imagine the real 30-day HV for the ES_30 contract will be different, but I'd assume I am within the general ballpark of how there would still be a decent discount).

Measuring and Mapping Implied Volatility

The next graph shows you the relative significance of various measurements of implied volatility within the ES_30 contract history. There are a lot of dots, but pay your attention to the segment for the E-Mini S&P 500 futures contracts.

Here, we are looking for extreme measurements of the current characteristics of the ES futures markets to see if there is any additional information we can potentially obtain. Here, we can see that the largest magnitude of historical movements is the turquoise-looking (that's a wild guess) dot, containing a z-score of -1.68. This means that this historical difference is relatively significant. This dot represents the 1-year at-the-money implied volatility within the ES_30 contact. Interpreting these, we can infer that the ATM 1-year implied volatility for the ES_30 contract is very low relative to historical standards, which gives us additional information, possibly relating to the relative cheapness of options-exposure via ES futures? Implied volatility is characterized as a rate variable, one in which does not trend, but exhibits clustering properties, as well as strong mean-reversion properties (just look at a VIX chart).

The below graph depicts the 1-week change in the at-the-money implied volatility term structure of ES futures contracts. One can clearly see that implied volatility is upward-sloping (consistent with that of the VIX index's current contango property), as well as how the current ES futures contract prices are in a state of backwardation (overall declining prices over time). This is meant to show how volatility derivatives traders have discounted aggregate volatility in the future relative to the past week.

Expected Moves

The below chart is a display, based on current market variables, of how participants are pricing in movements on an underlying ES futures contract to maturity, based upon previous volatility characteristics. For example, for the sake of consistency, we will analyze that of the E3AN21 ES futures contract which has 20 DTE, a 4,282 current spot price, at a 9.91% volatility estimation.

For summary statistics, it is estimated that, at the current level of volatility, roughly ~68%, ~95%, and ~99.7% of the time, this futures contract will finish between 4,183.64, 4,380.36 (-2.30%, 2.30%, 1 standard deviation), 4,088.62, 4,482.16 (-4.52%, 4.67%, 2 standard deviations), and 3,995.76, 4,586.32 (-6.68%, 7.11%, 3 standard deviations) by maturity.

One last thing. The below graph is simply meant to display historical patterns of incoming open-interest between a front-month and a subsequent-month ES future. Open interest, as a result of rolling from one contract to the next because of expiries with ES contracts, primarily floods into the subsequent contract when there is around 4-6 days-to-expiration on the front-month contract. So, if you hold a certain futures contract to maturity, do not be surprised if you see a lot more volume coming into the next contract towards the end of the lifecycle of the front-month contract.

Conclusion

Well, if you managed to read this entire blog post, good on you. I would not be surprised to see an increase in medium-term realized, and especially implied, volatility, as well as a relatively significant decrease in the price of the S&P 500. I have presented pricing arguments for contract selection, expected values of indexes, and contract pricings by expiration if one were to take on a hedge for such a scenario.

Comments

Post a Comment