In my previous post, the S&P 500 was at all-time-highs before dropping to almost -1.5% intraday as of this post. I highlighted how market participants, particularly those with superior information, were positioning for a moderate pullback in the short term. This post will explain the potential opportunity resulting from this pullback.

Displays April 26 - April 30, 2021 Data

Conclusion

Market Breadth

I would first like to mention a simple, yet power multi-factor model that incorporates price, volume, and volatility. As of today's close, the SPY's (an ETF that tracks the S&P 500 index) volume on today's poor performance (SPY rebounded from nearly -1.4% to -0.62%) accelerated against its previous trading day, 5 day volume average, 15 day volume average, 30 day volume average, as well as the 90 day volume average by +47.72%, +50.32%, +44.40%, +30.14%, and +29.69%, respectively, with the VIX index climbing by +6.39% to 19.48. This is what you do not want to see as a bullish investor with respect to volume by market participants. On bearish moments, one would desire volume to be decelerating on bearish days, not accelerating. It would be ideal for volume to fall on a rate-of-change basis, as well as the implied volatility for the security to be falling as well. Instead, price obviously fell, volume accelerated against ALL timeframe benchmarks, and forward-looking volatility implied by option prices accelerated by more than +6% on a 1 day timeframe, +9% on a 5 day average timeframe, and over 10% on a 15 day average timeframe. The top graph represents the VIX index, with the bottom being the SPY. This pullback might not be over in just 1 trading session.

It is extremely important to not only look at the absolute magnitude of changes in spot value of the prices of securities and indexes, but to also consider the relative derivative of said prices with respect to a variety of timeframes. This point of view can better help in timing market movements, as well as assessing the rate-of-change of a variety of market factors and whether the given movement is accelerating the existing trend.

Block Trade Order Flow the Past Few Days

As I outlined in my previous post, there was an obvious demand for market participants within the options on futures market on ES futures contracts for downside protection. Namely, OTM put options on their respective futures contracts. If one were tracking the amount of block trades within the futures market in relation to the S&P 500 index, it was extremely obvious that there was STILL massive demand for bearish derivative contracts. Posted below are the Equity Block Trade Summaries from April 29, 2021 through May 4, 2021.

One interesting takeaway from these block trades (>100 contracts in a single order) would be the manner in which the BTIC transactions took place. A BTIC order (Basis Trade at Index Close) allows one to trade futures at a fixed spread to the closing underlying index level. So, a negative price on a BTIC trade on the E-Mini S&P 500 futures contracts would represent how a buyer and a seller agreed on a fixed spread in which futures contracts would be delivered to the buyer at time of the trade closing. In a bullish market, one would desire a negative spread since it would be optimal, if one has a longer-term bullish view, to buy as low as possible by adding this fixed basis spread to the final underlying index value at the close of the current trading day. In a bearish market, it would be optimal to initiate a BTIC (or TACO, or TACO+, or BTIC+) with a positive fixed basis spread to be added to the final closing value of the underlying index at the end of the trade day. The reason is simply the inverse as above, if one were attempting to sell futures contracts as soon as possible, then it would be wise to sell at the highest price possible for the longer-term oriented trading view. This strategy can result index arbitrage strategies (calculate the fair value of the cash market for the index is significantly different than the spot level of the index), as well as hedging strategies that could be incorporated. So, the combination of short-term bearish derivatives trades with a longer-term BTIC viewpoint could reflect intelligent investors betting that this is a short-term pullback (hence the need for additional protection via a negative BTIC trade), while still positioning for accumulating shares for longer-term price appreciation of the S&P 500 index.

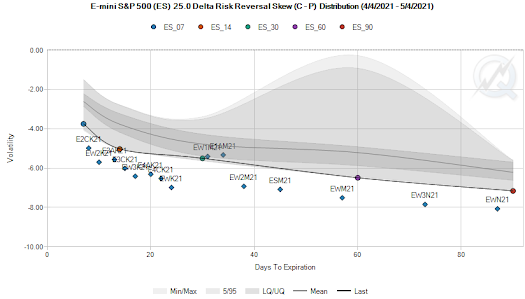

Implied Volatility Term Structure

When trading derivatives contracts, it is important to note the implied volatility term structure with respect to maturity as well as strike. For this first instance, we will reference the implied volatility term structure of a variety of futures derivatives contracts on the ES with respect to their ATM implied volatility value.

At first glance, it is extremely obvious that the ES futures contracts, derived from their respective options contracts, have an upward-sloping implied volatility curve. What this means is that dealers are quoting higher an higher prices (generally speaking) the farther out in time that the investor goes. Essentially, dealers are also simultaneously forecasting higher volatility for the ES futures market in the future. For the purposes of this post, the takeaway here is that, if one were to play a long futures contract if you were bullish on the S&P 500 (which I will explain why I am), it might be wise to play shorter-term maturity futures contracts, and then subsequently rolling these long contracts to later maturities for a lower average cost. In addition, the investor would also realize greater potential price appreciation since futures prices naturally converge towards the spot index value, allowing for greater positive variability in the futures contract. Another key takeaway is that it is now more expensive now to gain exposure to the S&P 500 via ES futures contracts than it was 7 days (noted by the higher orange line versus the non-dashed gray line). It might be wise to play an ES contract with no greater maturity than that of the ESM1. Furthermore, futures prices are in backwardation (evidence of a "normal" market), while the respective ATM implied volatilities are in contango.

Are Calls or Puts More Expensive than Last Week?

In terms of trying to target the ES futures contract that is closest to a 30 day maturity (to best mirror the VIX and other indexes I am tracking for consistency's sake) for a 25 delta options skew, this week puts are (on the ESM1 ES futures contract, has a DTE of 44.39) 26.7% rich while calls are 17.5% cheap relative to the ATM implied volatility value of the ESM1 futures contract. For context, calls were (on the EW3K1 ES futures contract, had a DTE of 20.86 at the time) 16.1% cheap and puts were 25.9% rich. This shows

Displays May 3 - May 4, 2021 Data

Displays April 26 - April 30, 2021 Data

I understand this short comparative analysis is a little bit of a stretch, but it, in my opinion, a simple and effective tool for gauging the relative change in price for call and put options on their respective futures contacts. The takeaway here is that call options are still relatively cheap if one were looking to gain some leveraged long exposure to the ES futures market (cheaper by magnitude of 920 basis points).

The VVIX and the VIX

As I have explained in previous posts, the relationship that the VVIX and the VIX have are of the upmost important. The VIX incorporates the implied volatility surface of OTM options contacts listed within the S&P 500 that meet the index's calculation methodologies and liquidity requirements, while the VVIX represents the implied volatility-of-volatility risk inherent in S&P 500 index option contacts. The VVIX contains risk premia that is not as present in S&P 500 options, such as the increased emphasis on jump risk (in diffusion models), accounting for sudden changes of price on an absolute magnitude basis. Because of this wholistic relationship the two have with one another, it is reasonable to assume that the VVIX index would front-run that of major moves taken on by the VIX, since it incorporates and emphasizes more risk factors (for more discussion on this, please see my post titled "Bumpier Times May Be Ahead"). Below are charts showing the VVIX and VIX indices on a 3 month time frame, respectively.

What is important to note here is the recent relative divergence in the rate-of-change between the two. The VIX rose by +6.39% from today's selloff, while the VVIX appreciated by only +2.68%. Now, considering the front-running nature of the VVIX index, it would appear that options markets are not pricing in extreme jumps in price, up or down. However, what is happening is how there will eventually be a point in which the VVIX will be flat on a given day (representing no change in expectation of potential magnitude of a price change within the S&P 500 index), while the VIX will appreciate marginally in value. At this moment, by utilizing a derivative framework in comparing the rates-of-change between the two indexes, we can better time a "topping" in increasing uncertainty with regards to future returns. Now, it would be different if the VVIX index began to strongly trend higher, but this has not happened.

Now that we can understand that volatility is not forecasted to accelerated to bearish means (this does not mean it will increase, just that it will slow in a derivative sense), we can begin looking for potential ways in which we can profit on this pullback. One more thing (that is less technical in nature). If there were serious demand for volatility products to either speculate on the bearish move for a new trend on not only price, but in the implied volatility space, the VIX and VVIX would not have collapsed -10.8% and -6%, respectively, from intraday highs to final daily closing values.

Initializing the Trade

Now that we can infer that there is not assumed to be a severe follow-through in forward-looking volatility, and because of that, realized volatility, one can ascertain a moderate bullish view on the markets, strictly based on the volatility complex of the ES futures contracts.

Long Futures/Call Options on Futures

One way in which we could express our belief that the S&P 500 is bullish in the medium/longer term (between 12-16 days and over 30 days) would be if we were to buy exposure through leveraging E-Mini S&P 500 futures contracts. The fact that they are leveraged allow the investor to control more shares than outright buying the index, allowing for a more cost-effective method in gaining bullish price exposure. Or, one could buy a call option on a specified futures contract that contain not only a relatively "cheap" implied volatility, but also sufficient liquidity needs.

This graph displays the ATM implied volatility distribution and a great visual on the future contact's previous distributions of said ATM implied volatility. As one can see, there has been an elevated average ATM implied volatility throughout the curve on a 1 month time series, with some futures contracts being below the respective constant ATM implied volatility interpolated through the ES futures contacts. This is important because, as we can all see, all futures contracts are well above their respective averages. This makes intuitive sense however, since the S&P 500 made 10 all-time-highs during the month of April. The important take away from this visual would be the futures contacts that have an ATM implied volatility below that interpolated ATM value, thereby presenting "relative" cheapness in buying a volatility product on the respective futures contract. In this instance, the one in which would be a good opportunity would be that of E4AK21, being that it is below this constant-maturity slope, as well as how it does not contain too large of a maturity in which we could not capture shorter-term opportunities as effectively. Another very important observation from the following visual would be the degree in which the cheapness of gaining long volatility exposure would be in the form of option contracts on these ES futures. As one can see, not only is the E4AK21 a "cheaper" ES contract, but also how its call options are relatively less expensive than a variety of other futures contracts' listed options (given by how put option on this contract have a considerable skew in the implied volatility smile) than a variety of other futures contracts.

Short Volatility

I understand that when an investor hears a short-volatility strategy, they instantly think of artificially inflated Sharpe ratios as well as the severe risk of tail events apparent in this general ecosystem. However, with the research above and in the previous post, we can begin to posit how implied volatility may react in the future. Will it rise sharply? Decline? Since we are bullish on the S&P 500 as a whole, as well as how we are bearish on the rate-of-change between the VIX and the VVIX (taking into account their critical relationship), we can theorize a decline in implied volatility in the future. One of the ways we can capture this viewpoint is the through the outright shorting of VIX futures contracts (could also long put options on these contracts for additional asymmetric leverage). This would not only benefit from the longer-term properties of contango between VIX futures contracts, but also between the accelerated decline of said VIX futures contracts if the VIX falls. Since VIX futures contracts are already within a contango ecosystem, they will rapidly converge to the VIX cash value upon maturity (it's like jumping out of a plane to catch a falling rock). This is very cost effective now with the introduction of VIX Micro Futures, with posting a little more than $1,200 the requirement for such a trade.

Another way we could gain short exposure to the VIX futures is through the purchasing of the SVXY ETF. This ETF aims to have a 30 day weighted average maturity of VIX futures contracts (consistent with VIX and UVXY) with a position of -0.5x the short-term VIX futures index. This means that this ETF aims to replicate inverse movements in VIX futures contracts by -0.5 times. This is beneficial because not only are we lesser-exposed to tail events, but also that it is often easier to simply buy an asset that "does the work for you" (a.k.a actively managing the rolling aspect to swinging futures contracts), rather than to actively manage a short position on futures contracts. This ETF recently began outperforming that of the SPY and has not looked back since, with its current share price being $49.50 (as of 5/4/2021 close).

The volatility markets within the S&P 500 index have popped higher today. This is not as much a signal for a new volatility regime, but it is more so, in my opinion, an episodic and non-trending movement in implied volatility. Volatility tends to cluster, as well as how it exhibits mean-reverting properties. Because of this, I would expect to see a "reversion to mean" towards a lower VIX value within the next couple of days. This represents an entry opportunity for the S&P 500 market (take advantage of emotional reactions to sell-offs) via ES contracts, the SPY, or a short-volatility trade via Micro VIX futures contacts, or the SVXY ETF. An initial target that I would have on a short VIX trade would be when the VIX corrects towards recent lows of 15.38, representing a potential decline of -21% in the index. Now, what's extremely important is if the VVIX does not create a new trend and begin to front-run the VIX index. If that happens, then I may possibly change my view.

Comments

Post a Comment